{kind=link}

Thanks a lot to @aerinykim, @suzatweet and @hardmaru for the useful feedback!

The academic Deep Learning research community has largely stayed away from the financial markets. Maybe that’s because the finance industry has a bad reputation, the problem doesn’t seem interesting from a research perspective, or because data is difficult and expensive to obtain.

In this post, I’m going to argue that training Reinforcement Learning agents to trade in the financial (and cryptocurrency) markets can be an extremely interesting research problem. I believe that it has not received enough attention from the research community but has the potential to push the state-of-the art of many related fields. It is quite similar to training agents for multiplayer games such as DotA, and many of the same research problems carry over. Knowing virtually nothing about trading, I have spent the past few months working on a project in this field.

This is not a “price prediction using Deep Learning” post. So, if you’re looking for example code and models you may be disappointed. Instead, I want to talk on a more high level about why learning to trade using Machine Learning is difficult, what some of the challenges are, and where I think Reinforcement Learning fits in. If there’s enough interest in this area I may follow up with another post that includes concrete examples.

I expect most readers to have no background in trading, just like I didn’t, so I will start out with covering some of the basics. I’m by no means an expert, so please let me know in the comments so if you find mistakes. I will use cryptocurrencies as a running example in this post, but the same concepts apply to most of the financial markets. The reason to use cryptocurrencies is that data is free, public, and easily accessible. Anyone can sign up to trade. The barriers to trading in the financial markets are a little higher, and data can be expensive. And well, there’s more hype so it’s more fun 🙂

Basics of Market Microstructure

Trading in the cryptocurrency (and most financial) markets happens in what’s called a continuous double auction with an open order book on an exchange. That’s just a fancy way of saying that there are buyers and sellers that get matched so that they can trade with each other. The exchange is responsible for the matching. There are dozens of exchanges and each may carry slightly different products (such as Bitcoin or Ethereum versus U.S. Dollar). Interface-wise, and in terms of the data they provide, they all look pretty much the same.

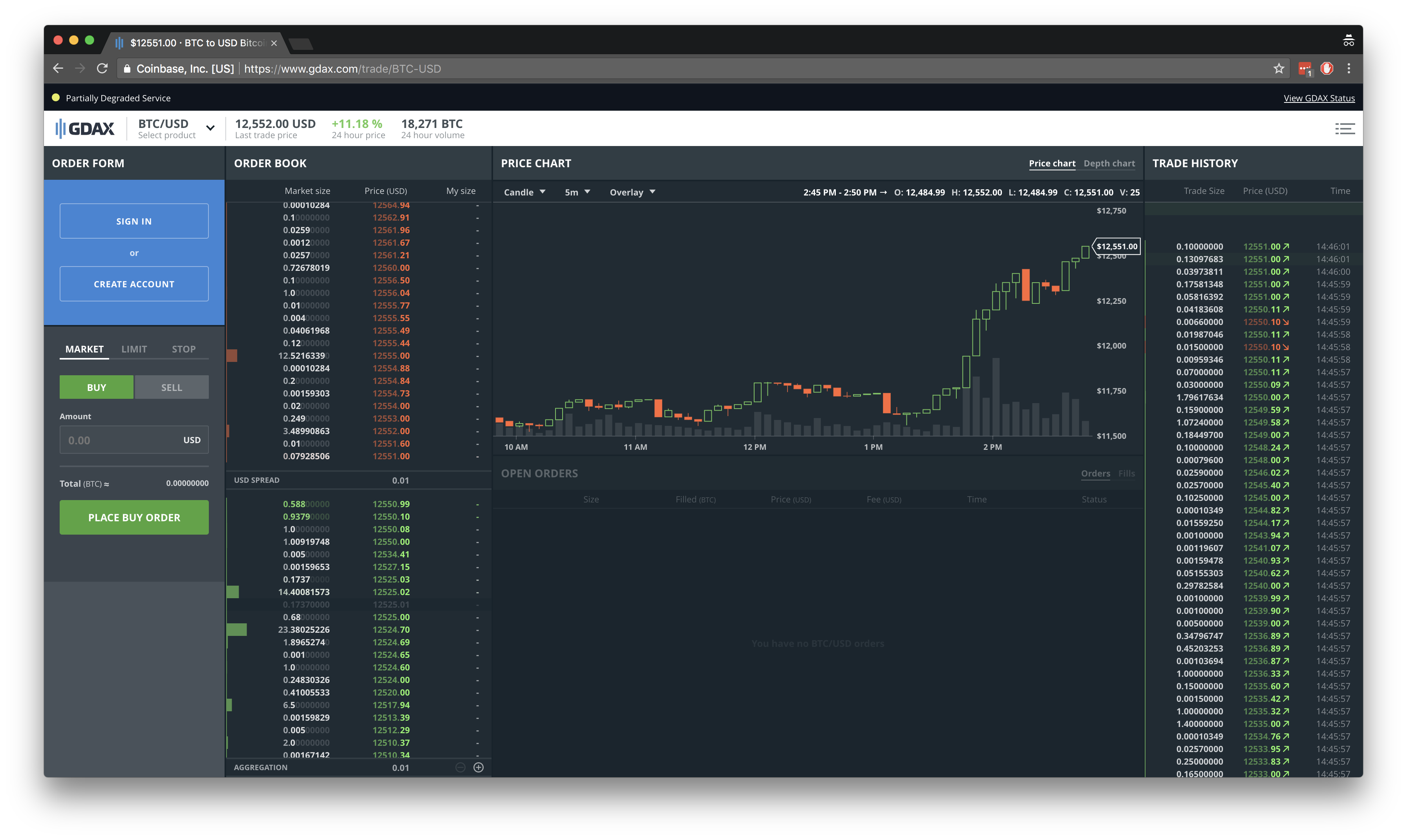

Let’s take a look at GDAX, one of the more popular U.S.-based exchanges. Let’s assume you want to trade BTC-USD (Bitcoin for U.S. Dollar). You would go to this page and see something like this:

There’s a lot of information here, so let’s go over the basics:

Price chart (Middle)

The current price is the price of the most recent trade. It varies depending on whether that trade was a buy or a sell (more on that below). The price chart is typically displayed as a candlestick chart that shows the Open/Start (O), High (H), Low (L) and Close/End (C) prices for a given time window. In the picture above, that period is 5 minutes, but you can change it using the dropdown. The bars below the price chart show the Volume (V), which is the total volume of all trades that happened in that period. The volume is important because it gives you a sense of the liquidity of the market. If you want to buy $100,000 worth if Bitcoin, but there is nobody willing to sell, the market is illiquid. You simply can’t buy. A high trade volume indicates that many people are willing to transact, which means that you are likely to able to buy or sell when you want to do so. Generally speaking, the more money you want to invest, the more trade volume you want. Volume also indicates the “quality” of a price trend. High volume means you can rely on the price movement more than if there was low volume. High volume is often (but not always, as in the case of market manipulation) the consensus of a large number of market participants.

Trade History (Right)

The right side shows a history of all recent trades. Each trade has a size, price, timestamp, and direction (buy or sell). A trade is a match between two parties, a taker and a maker. More on that below.

Order Book (Left)

The left side shows the order book, which contains information about who is willing to buy and sell at what price. The order book is made up of two sides: Asks (also called offers), and Bids. Asks are people willing to sell, and bids are people willing to buy. By definition, the best ask, the lowest price that someone is willing to sell at, is larger than the best bid, the highest price that someone is willing to buy at. If this was not the case, a trade between these two parties would’ve already happened. The difference between the best ask and best bid is called the spread.

Each level of the order book has a price and a volume. For example, a volume of 2.0 at a price level of $10,000 means that you can buy 2 BTC for $10,000. If you want to buy more, you would need to pay a higher price for the amount that exceeds 2 BTC. The volume at each level is cumulative, which means that you don’t know how many people, or orders, that 2 BTC consists of. There could one person selling 2 BTC, or there could be 100 people selling 0.02 BTC each (some exchanges provide this level of information, but most don’t). Let’s look at an example:

So what happens when you send an order to buy 3 BTC? You would be buying (rounding up) 0.08 BTC at $12,551.00, 0.01BTC at $12,551.6 and 2.91 BTC at $12,552.00. On GDAX, you would also be paying a 0.3% taker fee, for a total of about 1.003 * (0.08 * 12551 + 0.01 * 12551.6 + 2.91 * 12552) = $37,768.88and an average price per BTC of 37768.88 / 3 = $12,589.62. It’s important to note that what you are actually paying is much higher than $12,551.00, which was the current price! The 0.3% fee on GDAX is extremely high compared to fees in the financial markets, and also much higher than the fees of many other cryptocurrency exchanges, which are often between 0% and 0.1%.

Also note that your buy order has consumed all the volume that was available at the $12,551.00 and $12,551.60 levels. Thus, the order book will “move up”, and the best ask will become $12,552.00. The current price will also become $12,552.00, because that is where the last trade happened. Selling works analogously, just that you are now operating on the bid side of the order book, and potentially moving the order book (and price) down. In other words, by placing buy and sell orders, you are removing volume from the order book. If your orders are large enough, you may shift the order book by several levels. In fact, if you placed a very large order for a few million dollars, you would shift the order book and price significantly.

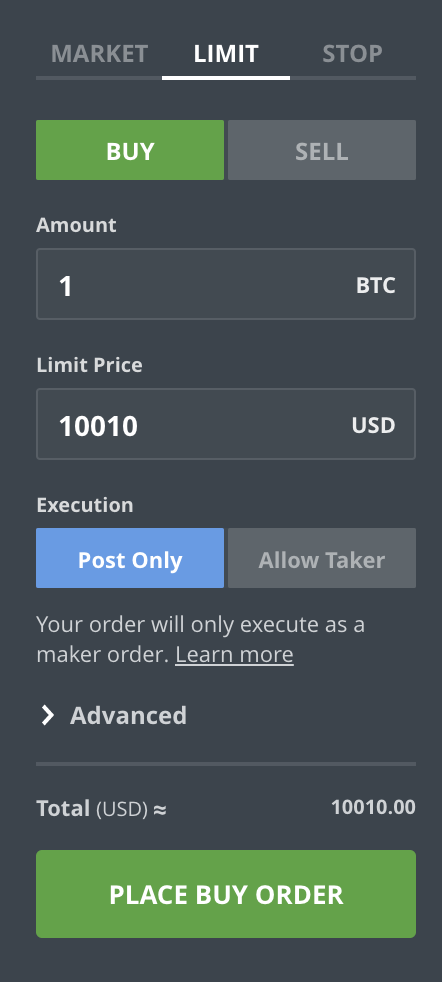

How do orders get into the order book? That’s the difference between market and limit orders. In the above example, you’ve issued a market order, which basically means “Buy/Sell X amount of BTC at the best price possible, right now“. If you are not careful about what’s in the order book you could end up paying significantly more than the current price shows. For example, imagine that most of the lower levels in the order book only had a volume at 0.001 BTC available. Most of your buy volume would then get matched at a much higher, more expensive, price level. If you submit a limit order, also called a passive order, you specify the price and quantity you’re willing to buy or sell at. The order will be placed into the book, and you can cancel it as long as it has not been matched. For example, let’s assume the Bitcoin price is at $10,000, but you want to sell at $10,010. You place a limit order. First, nothing happens. If the price keeps moving down your order will just sit there, do nothing, and will never be matched. You can cancel it anytime. However, if the price moves up, your order will at some point become the best price in the book, and the next person submitting a market order for a sufficient quantity will match it.

Market orders take liquidity from the market. By matching with orders from the order book, you are taking away the option to trade to from other people – there’s less volume left! That’s also why market orders, or market takers, often need to pay higher fees than market makers, who put orders into the book. Limit orders providing liquidity because they are giving others the option to trade. At the same time, limit orders guarantee that you will not pay more than the price specified in the limit order. However, you don’t know when, or if, someone will match your order. You are also giving the market information about what you believe the price should be. This can also be used to manipulate the other participants in the market, who may act a certain way based on the orders you are executing or putting into the book. Because they provide the option to trade and give away information, market makers typically pay lower fees than market takers. Some exchanges also provide stop orders, which allow you to set a maximum price for your market orders.

This was a very short introduction of how order books works and matching works. There are many more subtleties as well other, much more complex, order types. If the above was not clear, you can find a wealth of information about order book mechanics, and research in that area, through Google.

Data

The main reasons I am using cryptocurrencies in this post is because data is public, free, and easy to obtain. Most exchanges have streaming APIs that allow you to receive market updates in real-time. We’ll use GDAX (API Documentation) as an example again, but the data for other exchanges looks very similar. Let’s go over the basic types of events you would use to build a Machine Learning model.

Trade

A new Trade has happened. Each trade has a timestamp, a unique ID assigned by the exchange, a price, size, and side, as discussed above. If you wanted to plot the price graph of an asset, you would simply plot the price of all trades. If you wanted to plot the candlestick chart, you would window the trade events for a certain period, such as five minutes, and then plot the windows.

BookUpdate

One or more levels in the order book were updated. Each level is made up of the side (Buy=Bid, Sell=Ask), the price/level, and the new quantity at that level. Note that these are changes, or deltas, and you must construct the full order book yourself by merging them.

BookSnapshot

Similar to a BookUpdate, but a snapshot of the complete order book. Because the full order book can be very large, it is faster and more efficient to use the BookUpdate events instead. However, having an occasional snapshot can be useful.

That’s pretty much all you need in terms of market data. A stream of the above events contains all the information you saw in the GUI interface. You can imagine how you could make prediction based on a stream of the above events.

A few Trading Strategy Metrics

When developing trading algorithms, what do you optimize for? The obvious answer is profit, but that’s not the whole story. You also need to compare your trading strategy to baselines, and compare its risk and volatility to other investments. Here are a few of the most basic metrics that traders are using. I won’t go into detail here, so feel free to follow the links for more information.

Net PnL (Net Profit and Loss)

Simply how much money an algorithm makes (positive) or loses (negative) over some period of time, minus the trading fees.

Alpha and Beta

Alpha defines how much better, in terms of profit, your strategy is when compared to an alternative, relatively risk-free, investment, like a government bond. Even if your strategy is profitable, you could be better off investing in a risk-free alternative. Beta is closely related, and tells you how volatile your strategy is compared to the market. For example, a beta of 0.5 means that your investment moves $1 when the market moves $2.

Sharpe Ratio

The Sharpe Ratio measures the excess return per unit of risk you are taking. It’s basically your return on capital over the standard deviation, adjusted for risk. Thus, the higher the better. It takes into account both the volatility of your strategy, as well as an alternative risk-free investment.

Maximum Drawdown

The Maximum Drawdown is the maximum difference between a local maximum and the subsequent local minimum, another measure of risk. For example, a maximum drawdown of 50% means that you lose 50% of your capital at some point. You then need to make a 100% return to get back to your original amount of capital. Clearly, a lower maximum drawdown is better.

Value at Risk (VaR)

Value at Risk is a risk metric that quantifies how much capital you may lose over a given time frame with some probability, assuming normal market conditions. For example, a 1-day 5% VaR of 10% means that there is a 5% chance that you may lose more than 10% of an investment within a day.

Supervised Learning

Before looking at the problem from a Reinforcement Learning perspective, let’s understand how we would go about creating a profitable trading strategy using a supervised learning approach. Then we will see what’s problematic about this, and why we may want to use Reinforcement Learning techniques.

The most obvious approach we can take is price prediction. If we can predict that the market will move up we can buy now, and sell once the market has moved. Or, equivalently, if we predict the market goes down, we can go short (borrowing an asset we don’t own) and then buy once the market has moved. However, there are a few problems with this.

First of all, what price do we actually predict? As we’ve seen above, there is not a “single” price we are buying at. The final price we pay depends on the volume available at different levels of the order book, and the fees we need to pay. A naive thing to do is to predict the mid price, which is the mid-point between the best bid and best ask. That’s what most researchers do. However, this is just a theoretical price, not something we can actually execute orders at, and could differ significantly from the real price we’re paying.

The next question is time scale. Do we predict the price of the next trade? The price at the next second? Minute? Hour? Day? Intuitively, the further in the future we want to predict, the more uncertainty there is, and the more difficult the prediction problem becomes.

Let’s look at an example. Let’s assume the BTC price is $10,000 and we can accurately predict that the “price” moves up from $10,000 to $10,050 in the next minute. So, does that mean you can make $50 of profit by buying and selling? Let’s understand why it doesn’t.

- We buy when the best ask is $10,000. Most likely we will not be able to get all our 1.0 BTC filled at that price because the order book does not have the required volume. We may be forced to buy 0.5 BTC at $10,000 and 0.5 BTC at $10,010, for an average price of $10,005. On GDAX, we also pay a 0.3% taker fee, which corresponds to roughly $30.

- The price is now at $10,050, as predicted. We place the sell order. Because the market moves very fast, by the time the order is delivered over the network the price has slipped already. Let’s say it’s now at $10,045. Similar to above, we most likely cannot sell all of your 1 BTC at that price. Perhaps we are forced to sell 0.5 BTC are $10,045 and 0.5 BTC at $10,040, for an average price of $10,042.5. Then we pay another 0.3% taker fee, which corresponds to roughly $30.

So, how much money have we made? -10005 - 30 - 30 + 10,042.5 = -$22.5. Instead of making $50, we have lost $22.5, even though we accurately predicted a large price movement over the next minute! In the above example there were three reasons for this: No liquidity in the best order book levels, network latencies, and fees, none of which the supervised model could take into account.

What is the lesson here? In order to make money from a simple price prediction strategy, we must predict relatively large price movements over longer periods of time, or be very smart about our fees and order management. And that’s a very difficult prediction problem. We could have saved on the fees by using limit instead of market orders, but then we would have no guarantees about our orders being matched, and we would need to build a complex system for order management and cancellation.

But there’s another problem with supervised learning: It does not imply a policy. In the above example we bought because we predicted that the price moves up, and it actually moved up. Everything went according to plan. But what if the price had moved down? Would you have sold? Kept the position and waited? What if the price had moved up just a little bit and then moved down again? What if we had been uncertain about the prediction, for example 65% up and 35% down? Would you still have bought? How do you choose the threshold to place an order?

Thus, you need more than just a price prediction model (unless your model is extremely accurate and robust). We also need a rule-based policy that takes as input your price predictions and decides what to actually do: Place an order, do nothing, cancel an order, and so on. How do we come up with such a policy? How do we optimize the policy parameters and decision thresholds? The answer to this is not obvious, and many people use simple heuristics or human intuition.

A Typical Strategy Development Workflow

Luckily, there are solutions to many of the above problems. The bad news is, the solutions are not very effective. Let’s look a typical workflow for trading strategy development. It looks something like this:

- Data Analysis: You perform exploratory data analysis to find trading opportunities. You may look at various charts, calculate data statistics, and so on. The output of this step is an “idea” for a trading strategy that should be validated.

- Supervised Model Training: If necessary, you may train one or more supervised learning models to predict quantities of interest that are necessary for the strategy to work. For example, price prediction, quantity prediction, etc.

- Policy Development: You then come up with a rule-based policy that determines what actions to take based on the current state of the market and the outputs of supervised models. Note that this policy may also have parameters, such as decision thresholds, that need to be optimized. This optimization is done later.

- Strategy Backtesting: You use a simulator to test an initial version of the strategy against a set of historical data. The simulator can take things such as order book liquidity, network latencies, fees, etc into account. If the strategy performs reasonably well in backtesting, we can move on and do parameter optimization.

- Parameter Optimization: You can now perform a search, for example a grid search, over possible values of strategy parameters like thresholds or coefficient, again using the simulator and a set of historical data. Here, overfitting to historical data is a big risk, and you must be careful about using proper validation and test sets.

- Simulation & Paper Trading: Before the strategy goes live, simulation is done on new market data, in real-time. That’s called paper trading and helps prevent overfitting. Only if the strategy is successful in paper trading, it is deployed in a live environment.

- Live Trading: The strategy is now running live on an exchange.

That’s a complex process. It may vary slightly depending on the firm or researcher, but something along those lines typically happens when new trading strategies are developed. Now, why do I think this process is not effective? There are a couple of reasons.

- Iteration cycles are slow. Step 1-3 are largely based on intuition, and you don’t know if your strategy works until the optimization in step 4-5 is done, possibly forcing you to start from scratch. In fact, every step comes with the risk of failing and forcing you to start from scratch.

- Simulation comes too late. You do not explicitly take into account environmental factors such as latencies, fees, and liquidity until step 4. Shouldn’t these things directly inform your strategy development or the parameters of your model?

- Policies are developed independently from supervised models even though they interact closely. Supervised predictions are an input to the policy. Wouldn’t it make sense to jointly optimize them?

- Policies are simple. They are limited to what humans can come up with.

- Parameter optimization is inefficient. For example, let’s assume you are optimizing for a combination of profit and risk, and you want to find parameters that give you a high Sharpe Ratio. Instead of using an efficient gradient-based approach you are doing an inefficient grid search and hope that you’ll find something good (while not overfitting).

Let’s take a look at how a Reinforcement Learning approach can solve most of these problems.

Deep Reinforcement Learning for Trading

H20

Remember that the traditional Reinforcement Learning problem can be formulated as a Markov Decision Process (MDP). We have an agent acting in an environment. Each time step t the agent receives as the input the current state , St, takes an action At, and receives a reward R(t+1) and the next state S(t+1). The agent chooses the action based on some policy π: At = π(St). It is our goal to find a policy that maximizes the cumulative reward Σ^(Rt) over some finite or infinite time horizon.

Let’s try to understand what these symbols correspond to in the trading setting.

Agent

Let’s start with the easy part. The agent is our trading agent. You can think of the agent as a human trader who opens the GUI of an exchange and makes trading decision based on the current state of the exchange and his or her account.

Environment

Here it gets a little hairy. The obvious answer would be that the exchange is our environment. But the important thing to note is that there are many other agents, both human and algorithmic market players, trading on the same exchange. Let’s assume for a moment that we are taking actions on a minutely scale (more on that below). We take some action, wait a minute, get a new state, take another action, and so on. When we observe a new state it will be the response of the market environment, which includes the response of the other agents. Thus, from the perspective of our agent, these agents are also part of the environment. They’re not something we can control.

However, by putting other agents together into some big complex environment we lose the ability to explicitly model them. For example, one can imagine that we could learn to reverse-engineer the algorithms and strategies that other traders are running and then learn to exploit them. Doing so would put us into a Multi-Agent Reinforcement Learning (MARL) problem setting, which is an active research area. I’ll talk more about that below. For simplicity, let’s just assume we don’t do this, and assume we’re interacting with a single complex environment that includes the behavior of all other agents.

State

In the case of trading on an exchange, we do not observe the complete state of the environment. For example, we don’t know about the other agents are in the environment, how many there are, what their account balances are, or what their open limit orders are. This means, we are dealing with a Partially Observable Markov Decision Process (POMDP). What the agent observes is not the actual state St of the environment, but some derivation of that. Let’s call that the observation Xt, which is calculated using some function of the full state Xt ~ O(St).

In our case, the observation at each timestep t is simply the history of all exchange events (described in the data section above) received up to time t. This event history can be used to build up the current exchange state. However, in order for our agent to make decisions, there are a few other things that the observation must include, such as the current account balance, and open limit orders, if any.

Time Scale

We need to decide what time scale we want to act on. Days? Hours? Minutes? Seconds? Milliseconds? Nanoseconds? Variables scales? All of these require different approaches. Someone buying an asset and holding it for several days, weeks or months is often making a long-term bet based on analysis, such as “Will Bitcoin be successful?”. Often, these decisions are driven by external events, news, or a fundamental understanding of the assets value or potential. Because such an analysis typically requires an understanding of how the world works, it can be difficult to automate using Machine Learning techniques. On the opposite end, we have High Frequency Trading (HFT) techniques, where decisions are based almost entirely on market microstructure signals. Decisions are made on nanosecond timescales and trading strategies use dedicated connections to exchanges and extremely fast but simple algorithms running of FPGA hardware. Another way to think about these two extremes is in term of “humanness”. The former requires a big picture view and an understanding of how the world works, human intuition and high-level analysis, while the latter is all about simple, but extremely fast, pattern matching.

Neural Networks are popular because, given a lot of data, they can learn more complex representations than algorithms such as Linear Regression or Naive Bayes. But Deep Neural Nets are also slow, relatively speaking. They can’t make predictions on nanosecond time scales and thus cannot compete with the speed of HFT algorithms. That’s why I think the sweet spot is somewhere in the middle of these two extremes. We want to act on a time scale where we can analyze data faster than a human possibly could, but where being smarter allows us to beat the “fast but simple” algorithms. My guess, and it really is just a guess, is that this corresponds to acting on timescales somewhere between a few milliseconds and a few minutes. Humans traders can act on these timescales as well, but not as quickly as algorithms. And they certainly cannot synthesize the same amount of information that an algorithm can in that same time period. That’s our advantage.

Another reason to act on relatively short timescales is that patterns in the data may be more apparent. For example, because most human traders look at the exact same (limited) graphical user interfaces which have pre-defined market signals (like the MACD signal that is built into many exchange GUIs), their actions are restricted to the information present in those signals, resulting in certain action patterns. Similarly, algorithms running in the market act based on certain patterns. Our hope is that Deep RL algorithms can pick up those patterns and exploit them.

Note that we could also act on variable time scales, based on some signal trigger. For example, we could decide to take an action whenever a large trade occurred in the market. Such as trigger-based agent would still roughly correspond to some time scale, depending on the frequency of the trigger event.

Action Space

In Reinforcement Learning, we make a distinction between discrete (finite) and continuous (infinite) action spaces. Depending on how complex we want our agent to be, we have a couple of choices here. The simplest approach would be to have three actions: Buy, Hold, and Sell. That works, but it limits us to placing market orders and to invest a deterministic amount of money at each step. The next level of complexity would be to let our agent learn how much money to invest, for example, based on the uncertainty of our model. That would put us into a continuous action space, as we need to decide on both the (discrete) action and the (continuous) quantity. An even more complex scenario arises when we want our agent to be able to place limit orders. In that case our agent must decide the level (price) and the quantity of the order, bot